CleanSpark has signed a 20-year AI infrastructure lease, but still needs to finance an estimated $1.75 billion to $2.10 billion data center build.

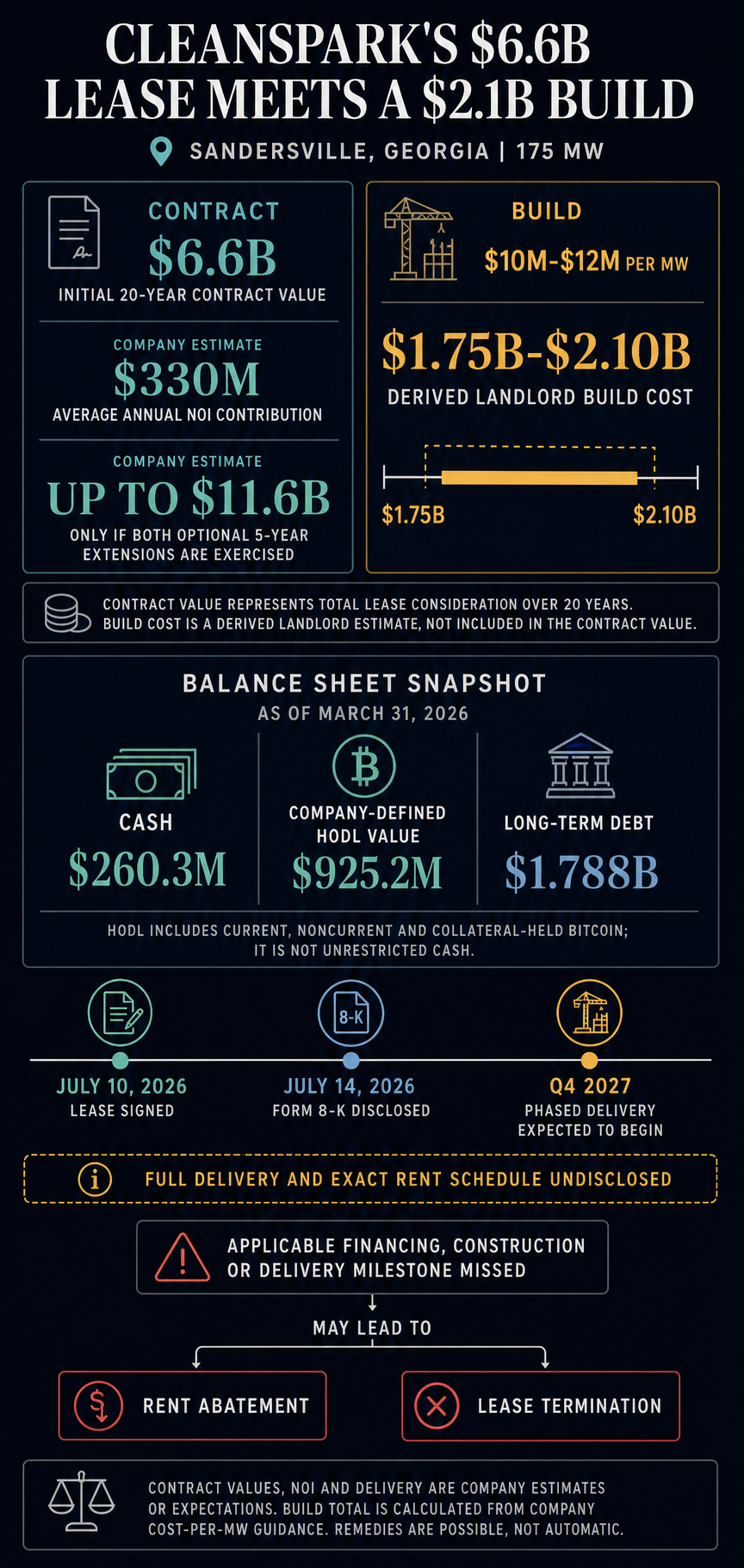

The Bitcoin miner and data center developer entered a 20-year triple-net lease for 175 megawatts of critical IT load at its Sandersville, Georgia, campus on July 10. CleanSpark disclosed the agreement in a Form 8-K on July 14 and estimates that the initial term will have a contract value of $6.6 billion and contribute about $330 million in average annual net operating income.

CleanSpark's estimate of $10 million to $12 million in landlord project costs per MW implies a $1.75 billion to $2.10 billion build.

That range exceeds the $260.3 million of cash and $925.2 million of company-defined Bitcoin HODL value reported as of March 31, 2026, even when the two figures are added together. The HODL measure includes current and noncurrent Bitcoin, as well as Bitcoin held by counterparties under collateral arrangements, a composition distinct from that of unrestricted cash.

The July lease announcement identifies no lender, committed financing amount, pricing, sponsor equity contribution, or draw schedule. Phased delivery is expected to begin in the fourth quarter of 2027, while the full delivery and rent-commencement schedules remain undisclosed. CleanSpark says the anonymous tenant's high-investment-grade credit profile facilitates access to financing. The eventual terms will determine whether the project is funded mainly against the lease or pushes more leverage, dilution or Bitcoin-collateral risk onto the company and its shareholders.

What CleanSpark actually signed

The Sandersville agreement is a binding infrastructure lease covering 175 MW, with annual escalators, a 20-year initial term and two optional five-year extensions. The tenant is described only as a high-investment-grade global technology company, with its identity undisclosed.

CleanSpark estimates $6.6 billion in contract value during the initial term and up to $11.6 billion if both five-year options are exercised. The initial signed term remains $6.6 billion; reaching $11.6 billion requires exercise of both options.

Calling it a triple-net lease does not mean CleanSpark is also on the hook to build the project. The 8-K states that the tenant bears the costs, charges, indemnities, and expenses specified in the lease. CleanSpark separately estimates the landlord project costs at $10 million to $12 million per MW in the SEC-filed release, resulting in a calculated range of $1.75 billion to $2.10 billion for 175 MW.

Item Amount or timing What it represents Initial contract value $6.6 billion CleanSpark estimate over the 20-year initial term Value with extensions Up to $11.6 billion Only if both five-year tenant options are exercised Average annual NOI contribution About $330 million Company estimate for prospective income Landlord project cost $1.75 billion to $2.10 billion Calculated from the company's $10 million to $12 million per MW estimate March 31 balance sheet $260.3 million cash; $925.2 million HODL value; $1.788 billion long-term debt Dated financial position; excludes Sandersville financing terms Delivery Expected to begin Q4 2027 Phased start; full completion and exact rent schedule undisclosed

The contract value is spread over years, while the estimated NOI remains prospective. A phased construction program may also not require the entire project cost upfront. The figures establish the scale of the obligation without revealing when each dollar must be funded.

The funding paths move risk differently

CleanSpark's fiscal second-quarter results show why Sandersville needs funding that matches the scale of the build.

As of March 31, the company reported $260.3 million in cash, $925.2 million in HODL value, $1.788 billion in long-term debt, and $1.927 billion in total liabilities. The calculated Sandersville cost is approximately 6.7 to 8.1 times the dated cash balance, 1.9 to 2.3 times the HODL value, and roughly 98% to 117% of long-term debt. These figures show that the project is simply too big for CleanSpark to fund with its existing cash.

CleanSpark also reported a $378.3 million net loss for the quarter ended March 31. The figure included a $224.1 million Bitcoin fair-value loss and a $38.8 million loss on Bitcoin collateral, according to its SEC-filed earnings release. Those market-linked items can significantly affect the reported balance sheet, making the net loss a poor proxy for quarterly cash burn.

Bitcoin remains a potential source of liquidity, collateral, or sale proceeds, depending on how much is encumbered and the level of exposure the company wants to retain. Coins pledged to a lender cannot also function as an unencumbered reserve. CryptoSlate previously examined how collateral-held Bitcoin complicates the liquidity implied by CleanSpark's headline HODL figure.

One plausible scenario is project financing built around the site and its tenant-backed lease. CleanSpark says the tenant's credit profile facilitates financing options, and a long-duration lease may provide lenders with a contractual cash-flow basis for underwriting construction. The protections would depend on the actual package: sponsor guarantees, corporate recourse, Bitcoin collateral, or a large sponsor equity commitment could move risk back to CleanSpark.

The lease ties financing directly to CleanSpark's ability to deliver the project. CleanSpark's 8-K states that the company must meet applicable financing, construction, and delivery milestones, as well as other covenants and conditions. Miss a milestone and the rent could shrink or disappear entirely, leaving the project's financing tied to CleanSpark keeping the lease on track.

Funding Sandersville through CleanSpark's corporate balance sheet would expose shareholders more directly to the cost. Additional corporate debt would raise leverage from a March 31 base of nearly $1.8 billion in long-term debt. New common equity or equity-linked securities could dilute existing holders. Bitcoin sales would reduce treasury exposure and the asset base investors may count as liquidity. Bitcoin-backed borrowing could preserve nominal coin ownership while adding collateral, margin, and liquidation risk.

CleanSpark's $1.769 billion net carrying balance for zero-coupon convertible notes represents outstanding debt. Its $400 million in unused Bitcoin-backed credit lines were undrawn as of March 31 and require Bitcoin collateral. CryptoSlate's coverage of the 2025 convertible financing gives context for the corporate route, while Hut 8's AI landlord model illustrates how project debt and Bitcoin-backed bridge capital can coexist. CleanSpark's eventual structure remains an open question.

The tenant's credit profile may support project financing, but the eventual pricing, recourse, collateral, and equity requirements will determine how much risk remains with CleanSpark.

Why the $6.6 billion value remains conditional

The $6.6 billion headline still comes with strings attached. The financing, construction, delivery, and other milestones and covenants disclosed in the 8-K link the revenue opportunity to CleanSpark's ability to execute. The remedies are conditional: the filing states that applicable failures may result in rent abatements or termination.

The timeline adds another catch. CleanSpark expects phased deliveries to begin in Q4 2027. It has not disclosed how quickly the full 175 MW will follow, when rent begins for each phase, or whether the stated average annual NOI reflects a fully delivered campus. Using $330 million as a run-rate from the first day of Q4 2027 would overstate the disclosed timing.

The Texas deal is not part of CleanSpark's signed contract pipeline. The same tenant executed a letter of intent and exclusivity agreement covering CleanSpark's 718-acre Texas portfolio and up to 885 MW of what CleanSpark describes as secured and planned power capacity. That arrangement is not a completed lease.

Sandersville has advanced CleanSpark from an AI infrastructure pitch to contracted execution, while the decisive capital terms remain undisclosed.

The financing terms and the path to Q4 2027 will reveal who is really carrying the risk: CleanSpark's Bitcoin holdings, its balance sheet, or its shareholders.